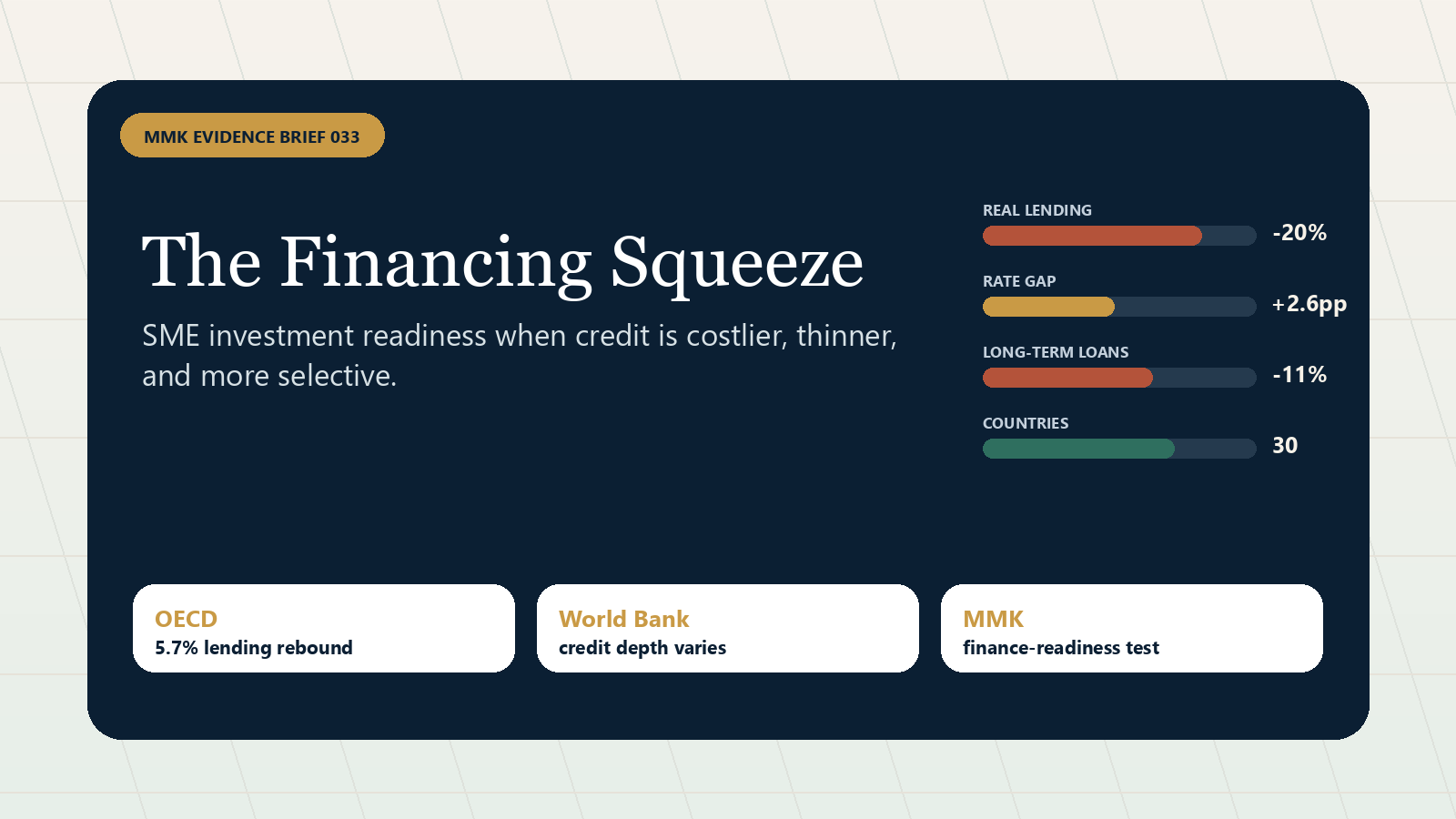

OECD's 2026 SME-finance evidence shows a recovery with a warning label. New SME lending grew by 5.7% in 2024 after a 9% decline in 2023, yet aggregate new SME lending in real terms was still 20% below 2019 in selected countries. Average SME interest rates remained 2.6 percentage points above 2019, and aggregate long-term SME loan volumes had declined 11% since 2021.

In Brief

What changed. The credit window has not closed, but lenders are still pricing risk hard. OECD's 31 March 2026 report shows lending recovery, higher financing costs, shorter horizons, and falling SME loan share in 30 Scoreboard countries.

Why it matters. SMEs cannot treat funding as a last-minute request. In a selective market, the firms that can show clean financials, realistic cash forecasts, collateral logic, demand evidence, and repayment capacity will move faster.

What leaders should do. Build the finance-readiness folder before the business needs money: use-of-funds logic, cash-flow stress tests, margin analysis, debtor ageing, management accounts, covenant watchpoints, and a short lender or investor memo.

The Signal

The headline recovery in lending does not remove the squeeze. OECD's data show that SME lending can grow in nominal terms while the real lending flow remains below its pre-shock baseline. That difference matters for firms facing higher input costs, currency pressure, and slower customer payment cycles. A business can hear that lending is recovering and still find that its own loan offer is smaller, more expensive, more secured, or shorter than planned.

The wider macro setting reinforces that caution. The World Bank's June 2026 Global Economic Prospects report sets global growth at 2.5% for 2026 and says private investment growth in developing economies in the 2020s has more than halved compared with the 2010s. The IMF's April 2026 Global Financial Stability Report warns that tighter financial conditions remain a risk, especially for emerging markets that are exposed to shifting risk sentiment and capital flows.

Why The Squeeze Hits Investment First

Working-capital credit and investment credit are not the same problem. Working capital keeps stock, payroll, and receivables moving. Investment credit asks the lender to believe in tomorrow's demand, margin, execution, and repayment capacity. When rates remain high and long-term loan volumes fall, the first casualty is often growth investment: equipment, expansion, inventory depth, new locations, technology, and export preparation.

That is why a financing squeeze can slow businesses even when the loan market is technically open. The issue is not only access. It is the quality of access: price, tenor, security, documentation burden, and lender confidence in the borrower.

Credit Depth Changes The Local Test

Financing conditions are not uniform across African markets. World Bank WDI data show large differences in domestic credit to the private sector by banks as a share of GDP. In the selected markets below, South Africa's latest available value is 57.5% of GDP, Kenya is 29.7%, Egypt is 27.6%, Nigeria is 13.1% using 2023 because the 2024 API value was unavailable, and Ghana is 8.3%.

For SMEs, that means the same business case can face different financing frictions by market. Where private-credit depth is lower, firms often need stronger internal evidence, a clearer repayment story, and a more realistic funding ladder: supplier credit, retained earnings, bank working capital, equipment finance, grants, development-finance facilities, or equity-like capital.

The Extra Test: Four Signals To Watch Together

The most useful reading is not any single metric. It is the pattern. Real new SME lending below 2019, rates above the pre-tightening baseline, weaker long-term loan volumes, and a falling SME share of outstanding loans all point in the same direction: lenders are still separating stronger borrowers from weaker ones.

Evidence Box

New SME lending grew 5.7% in 2024 after a 9% decline in 2023, but real new SME lending was still 20% below 2019 in selected countries.

Source: OECD Financing SMEs and Entrepreneurs 2026, published 31 March 2026 The flow improved, but the real purchasing power of SME credit remains weaker than the pre-shock baseline.Average SME interest rates remained 2.6 percentage points above 2019, aggregate long-term SME loan volumes were 11% lower than in 2021, and SME loan share declined in 30 Scoreboard countries.

Source: OECD Financing SMEs and Entrepreneurs 2026, Recent trends chapter Borrowers face a price-and-tenor problem, not only an approval problem.World Bank WDI data show domestic credit to the private sector by banks at 57.5% of GDP in South Africa, 29.7% in Kenya, 27.6% in Egypt, 13.1% in Nigeria using 2023 latest available, and 8.3% in Ghana.

Source: World Bank WDI indicator FD.AST.PRVT.GD.ZS; API last updated 8 April 2026 Lower private-credit depth raises the importance of strong borrower documentation and diversified funding routes.The World Bank's June 2026 Global Economic Prospects report forecasts global growth at 2.5% in 2026 and says private investment growth in developing economies in the 2020s has more than halved compared with the 2010s.

Source: World Bank Global Economic Prospects, June 2026 PDF The financing squeeze sits inside a broader weak-investment environment.The IMF's April 2026 Global Financial Stability Report says financial-stability risks remain elevated and warns that tighter financial conditions remain a risk.

Source: IMF Global Financial Stability Report, April 2026 Emerging-market borrowers should expect investor and lender scrutiny to remain sensitive to global risk sentiment.What SMEs And Advisors Should Do Now

- Separate survival finance from investment finance. A working-capital bridge, equipment loan, expansion loan, and equity round each need different evidence, repayment logic, and risk allocation.

- Prepare the borrower file before approaching lenders. Include management accounts, bank statements, debtor and creditor ageing, tax status, use-of-funds schedule, current debt, collateral position, and signed customer or supplier evidence where available.

- Build a 13-week cash view and a 12-month stress test. Show what happens if revenue is delayed, input costs rise, FX moves, a key debtor pays late, or the loan rate is higher than expected.

- Prove repayment capacity, not just ambition. Lenders and investors need to see recurring demand, margin discipline, working-capital cycles, and management controls that protect cash.

- Use a funding ladder. Match the instrument to the job: supplier terms for stock timing, invoice finance for receivables, equipment finance for assets, grants for public-good components, and patient capital for expansion risk.

- Convert the case into a short decision memo. The best funding conversations are easier because the borrower has already translated the business into the language of credit, risk, and return.

What To Watch Next

Track four signals through the second half of 2026: updated central-bank rate paths, bank lending surveys, SME arrears and default indicators, and the next WDI/enterprise-survey updates on credit access. If inflation and policy rates ease but lender appetite stays cautious, borrower evidence will still decide who receives usable capital.

MMK advisory angle. MMK Consult helps SMEs, funders, founders, and institutions convert business plans into finance-ready evidence: lender packs, investor memos, cash-flow models, market validation, risk notes, use-of-funds logic, and board-ready financing decisions. The goal is simple: make the next funding conversation specific, defensible, and decision-ready.

Sources

- OECD — Financing SMEs and Entrepreneurs 2026, Recent trends chapter, published 31 March 2026

- World Bank WDI — Domestic credit to private sector by banks (% of GDP), indicator FD.AST.PRVT.GD.ZS

- World Bank API extract used for Figure 3

- World Bank — Global Economic Prospects, June 2026 PDF

- IMF — Global Financial Stability Report, April 2026

- AfDB — African Economic Outlook 2026