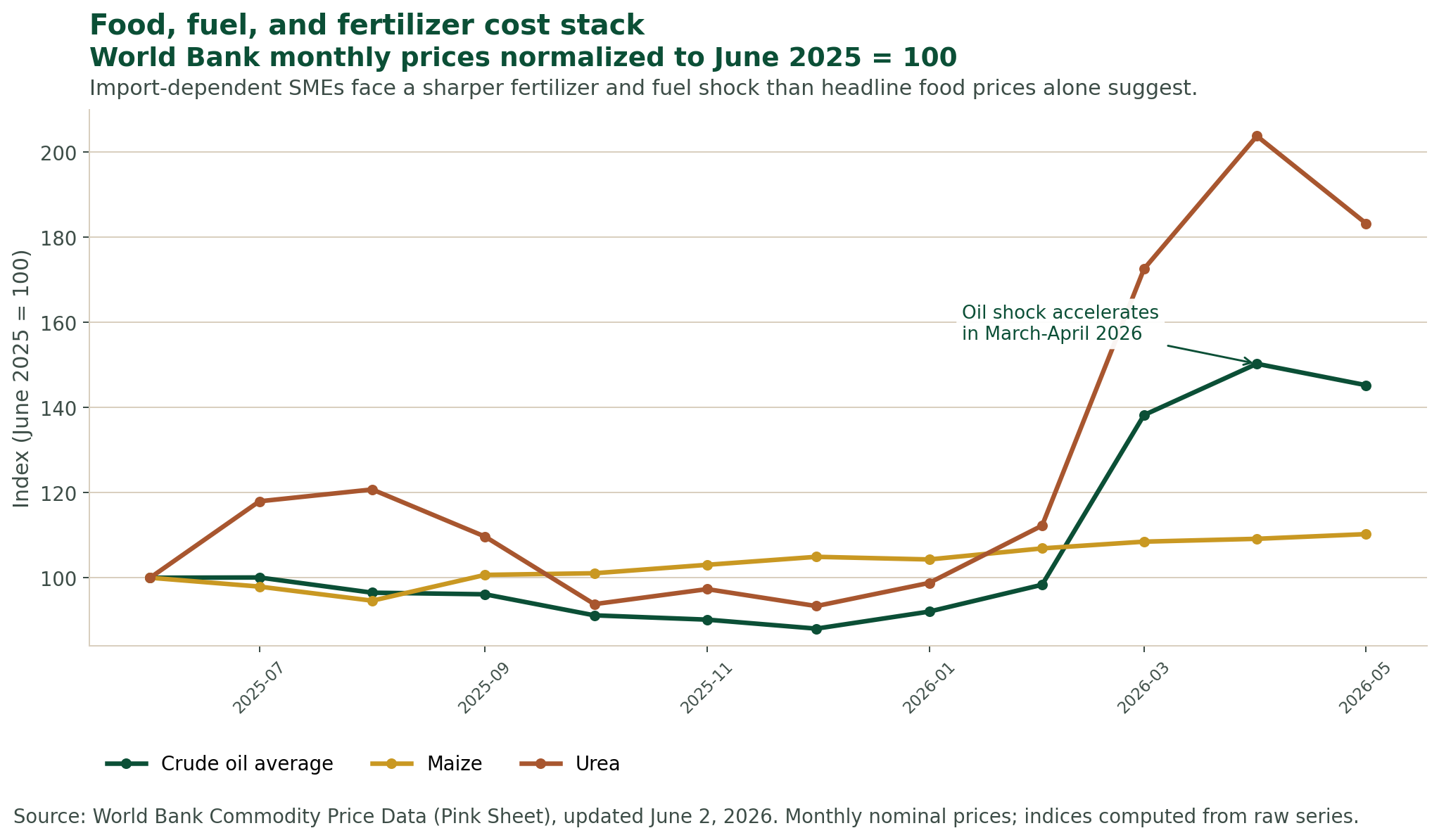

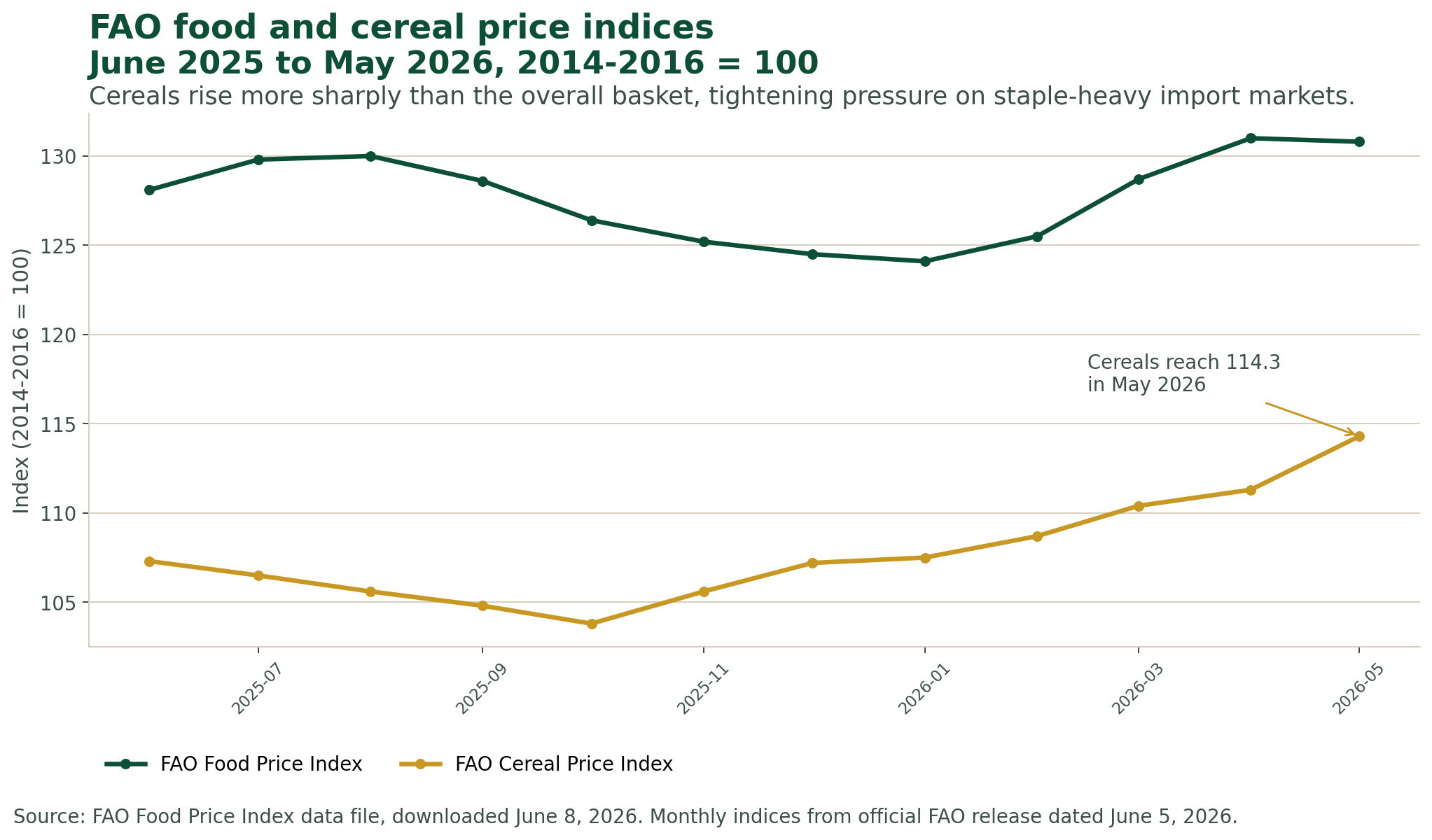

Between June 2025 and May 2026, World Bank monthly price data show urea up 83.2%, crude oil up 45.2%, and maize up 10.3%. Over the same period, FAO's cereal price index climbed from 107.3 to 114.3. For import-dependent SMEs, this is not abstract macroeconomics. It is a direct margin squeeze hitting transport, procurement, packaging, food inputs, and working capital at the same time.

In Brief

- What changed. The latest World Bank and FAO releases show a renewed cost-of-living shock in the parts of the basket that matter most to import-dependent SME economics: energy, fertilizer, and staples.

- Why it matters. SMEs typically have weaker pricing power, thinner buffers, and less flexible financing than large firms. A simultaneous rise in transport, input, and staple costs compresses margins faster than many small businesses can adjust.

- What leaders should do. Reprice faster, protect working capital, separate high-margin from low-margin lines, renegotiate procurement assumptions, and track gross margin weekly instead of waiting for month-end surprises.

The Signal

World Bank commodity data show the shock is not evenly distributed. The steepest movement is in fertilizer and fuel, with food grains rising more steadily in the background. That matters because import-dependent SMEs often absorb these categories through several channels at once: transport costs, supplier price resets, food procurement, packaging, and customer demand weakness.

The FAO Food Price Index release dated 5 June 2026 adds another layer. The overall basket is not exploding, but cereals continue to move higher. For businesses operating in food-linked retail, light manufacturing, hospitality, distribution, and household consumer markets, the cereal trend matters more than a broad average because it feeds directly into staple affordability and demand pressure.

What The Evidence Suggests

The World Bank's April 2026 Commodity Markets Outlook says the fertilizer index is projected to rise by more than 30% in 2026 and warns that fertilizer affordability is expected to deteriorate to the worst levels since 2022, pressuring farming profit margins. That is the upstream version of the SME problem: when farming, transport, and imported input costs worsen together, downstream businesses inherit the squeeze.

The IMF's Sub-Saharan Africa Regional Economic Outlook of 16 April 2026 says the region's 2026 growth forecast has been cut to 4.3% and links the downgrade to the latest external shocks, especially higher fuel and fertilizer prices. An IMF policy note published on 20 May 2026 adds that imported-energy economies can lose 2-3% of GDP in real income under this kind of shock. That is the macro backdrop for weaker customers, tighter cash flow, and more conservative spending.

OECD's Financing SMEs and Entrepreneurs 2026 adds the financing side of the story. Borrowing costs were easing at the margin, but the report says they remain historically high, with 34 out of 39 countries still showing higher SME rates than before the pandemic. In plain terms: even if cost pressure is temporary, many smaller firms do not have cheap capital to bridge the period safely.

What This Means For Your Business

If your business imports directly, depends on imported distributors, or sells into households already stretched by food and transport costs, the wrong response is to wait for inflation headlines to settle. The more useful question is narrower: which line items are moving now, how quickly are suppliers repricing them, and where is your gross margin exposed first?

For many SMEs, the danger is not one dramatic shock. It is the slow accumulation of smaller pressures: transport is up, one key input is up, customers trade down, and receivables take longer to collect. The result is a working-capital problem that looks operational on the surface but is really a pricing and margin problem underneath.

Evidence Box

Urea rose 83.2% from June 2025 to May 2026.

Source: World Bank Commodity Price Data (Pink Sheet), updated 2 June 2026 The fertilizer shock is the sharpest part of the stack and can feed through to food systems, farm inputs, and downstream SME costs.Crude oil rose 45.2% and maize 10.3% over the same period.

Source: World Bank Commodity Price Data (Pink Sheet), updated 2 June 2026 Transport-intensive and food-linked SMEs face a dual squeeze: higher delivery costs and higher staple input costs.FAO's cereal index rose from 107.3 in June 2025 to 114.3 in May 2026.

Source: FAO Food Price Index release dated 5 June 2026 The staple component is moving faster than the overall basket, which matters more for household demand and food-facing SMEs.SME borrowing costs remain historically high, with 34 of 39 countries still above pre-pandemic rates.

Source: OECD Financing SMEs and Entrepreneurs 2026 A margin shock is harder to absorb when bridging finance is still expensive.Imported-energy economies can lose 2-3% of GDP in real income under the latest energy-food shock.

Source: IMF policy note, 20 May 2026 This is not just a cost issue. It is also a demand and liquidity issue for businesses serving already stretched markets.Practical Actions

- Build a weekly margin sheet. Track gross margin by product line, not just total sales. Rising revenue can hide weakening unit economics.

- Reprice in smaller, faster moves. One large annual reset is too slow when supplier costs are changing monthly. Shorter review cycles reduce shock and customer backlash.

- Protect cash before growth. Tighten stock discipline, shorten receivable cycles where possible, and avoid financing low-margin inventory with expensive short-term borrowing.

- Separate strategic customers from unprofitable volume. In a squeeze, not every sale is worth keeping. Focus on customers, channels, and products that defend contribution margin.

- Stress-test your imported input assumptions. Update oil, fertilizer, shipping, and FX scenarios together. A single-input forecast is too optimistic in a stacked-cost environment.

What To Watch Next

Watch three things closely over the next quarter: whether fertilizer affordability worsens further, whether fuel pressure keeps filtering into transport and distribution invoices, and whether food-importing governments respond with tax, subsidy, or FX measures that shift pass-through dynamics. For SMEs, those policy choices can matter almost as much as the commodity move itself.

MMK advisory angle. MMK Consult helps businesses and institutions convert macro pressure into decision-ready action: pricing reviews, margin diagnostics, market intelligence, feasibility work, customer research, and evidence-led strategy notes. The objective is not to narrate the shock. It is to identify what your business should change before the shock reaches the income statement in full.

Sources

- FAO - Food Price Index release and data file, 5 June 2026

- World Bank - Commodity Price Data (Pink Sheet), updated 2 June 2026

- World Bank - Commodity Markets Outlook, April 2026

- World Bank - Fertilizer prices surge as Strait of Hormuz disruptions tighten, 14 May 2026

- IMF - Regional Economic Outlook for Sub-Saharan Africa, 16 April 2026

- IMF - Responding to the energy and food price shock, 20 May 2026

- OECD - Financing SMEs and Entrepreneurs 2026